With a presidential election looming, geopolitical tensions escalating, and central banks considering a significant shift in its policy stance, 2024 looks to be an eventful year with many possible outcomes. So far, the financial markets are taking a “what, me worry?” attitude, as stock prices have hit new records and businesses have had little trouble raising huge amounts of funds in the capital markets. One reason for market complacency is that unfolding developments and the swirl of uncertainty facing the nation have hardly put a dent in the economy. The job market is still chugging along, incomes are rising amid easing inflation, consumers are grumbling about high prices and interest rates but continue to spend, and household and business balance sheets are in good shape.

Simply put, recession fears that were so rampant last year have been put on the back burner as the economy seems able to weather anything thrown at it, including a pandemic, wars, inflation, and skyrocketing interest rates since the spring of 2022. A sense of invincibility, however, is not an effective weapon against adversity. Indeed, history shows that the economy usually appears strong in the months before a recession strikes, much like the current backdrop. But when things start to go bad, they tend to go bad quickly and are difficult to stop. That’s not to say a burst of misfortune is inevitable. A soft landing where the stars align to bring about sustained growth, high employment, and low inflation may well be in store for the U.S. economy; indeed, many more commentators believe that such a Goldilocks scenario has a chance of materializing than a few months ago.

But luck, as well as intelligent decisions, will need to play a role in the process. Luck would involve easing Middle East tensions, limited economic ramifications from the Russia/Ukraine conflict, and a calm political process leading up to the November elections. Smart decisions will also be required of policymakers who are debating when and by how much to cut interest rates this year. However, smart decisions mean that the Federal Reserve needs reliable data to guide it, which may be difficult to obtain early in the year. That’s when incoming data are corrupted by unpredictable winter weather and the resetting of prices and wages that may temporarily give a distorted picture of underlying inflation and income trends. Policymakers are not flying blind, but any misinterpretation of reality due to faulty information can lead to misguided policy decisions that have harmful economic effects down the road. Hopefully, spring will bring more clarity to the economy before it is too late.

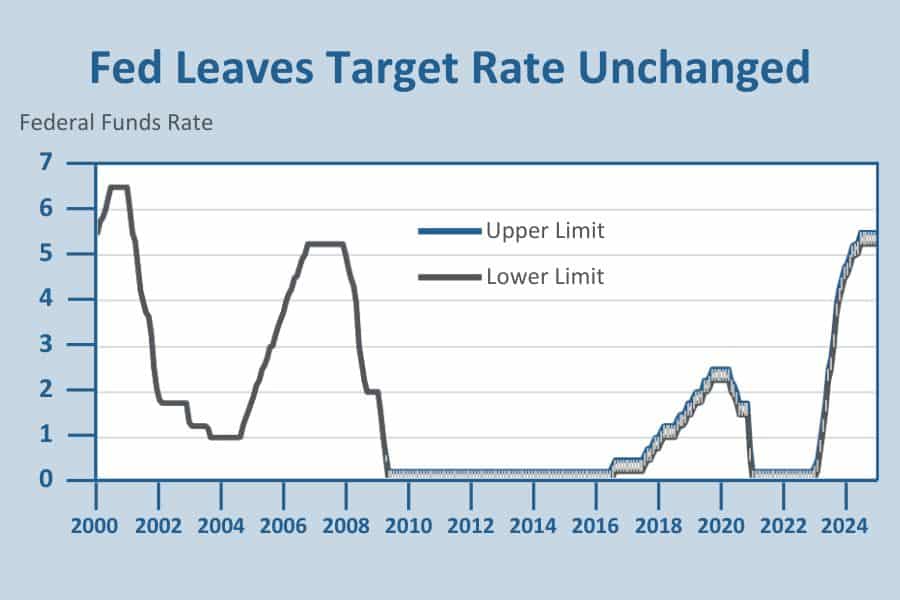

The Fed Stays the Course

In the waning months of 2023, most economists thought the economy was poised to roll over and would need the Fed to step in quickly to stave off a recession. After all, inflation had tumbled dramatically over the year’s second half, and the 2% target sought by policymakers seemed well within reach. Slowing growth, the ongoing healing of supply chain bottlenecks, and the potential bite from the Fed’s aggressive rate hiking campaign were coalescing into a receptive backdrop for the Fed to start cutting rates sooner rather than later.

However, as the calendar turned to 2024, some key data refused to follow the script. Both job creation and inflation came in hotter than expected in January and February, prompting the markets to rethink the wisdom of a growth-stimulating rate cut. To their credit, the Fed had steadfastly resisted calls for an imminent rate cut, clashing with traders who were pricing in not only an early reduction in rates but a total of 6 before the end of the year. However, following the data for January and February, that divide between the Fed and the markets has closed; for the first time in a while, traders and policymakers are on the same page.

Unsurprisingly, at the March 19-20 policy meeting, Fed officials reaffirmed their “wait-and-see” approach, keeping the policy rate unchanged at the 5.25-5.50% range in place since last July. Also, unsurprisingly, the markets applauded this stand-pat approach, recognizing that the risk of stoking higher inflation was just as high as the risk of bringing on a recession. In their updated projections, Fed officials still expect to cut rates three times this year, but the starting date remains up in the air.

Showing Patience

As always, the Fed is being data-dependent. As Chair Powell reiterated at his post-meeting press conference, inflation is moving in the right direction (down) but not as quickly as hoped. By itself, that won’t derail the predicted rate cuts; inflation does not have to hit the 2% target for the Fed to pull the rate-cutting trigger. It only needs to show it is moving sustainably towards that goal. Unfortunately, the data over the first two months of the year suggest that progress on the inflation front may have stalled as both consumer and producer prices (the cost of goods to businesses) ticked higher.

Moreover, as noted earlier, job growth also came in stronger than expected. That, in turn, creates more paychecks, which should support demand and allow businesses to keep raising prices. No doubt, both the strength in the job market and hotter consumer price data have given the Fed less confidence that inflation will continue to retreat, something that Chair Powell noted in his post-meeting press conference on March 20.

But just as the Fed did not respond in knee-jerk fashion to the steep inflation retreat in 2023 by cutting interest rates, they are not about to overreact to two months of firmer-than-expected price data by turning more hawkish. As Powell noted, it is still being determined if the uptick in inflation in January and February is just a bump in the road or something more persistent. Since Fed officials did not change their December prediction of three rate cuts this year, they still believe the inflation retreat will resume in the coming months. The road will be bumpier, but the last mile to 2% was always considered the hardest.

Questioning the Data

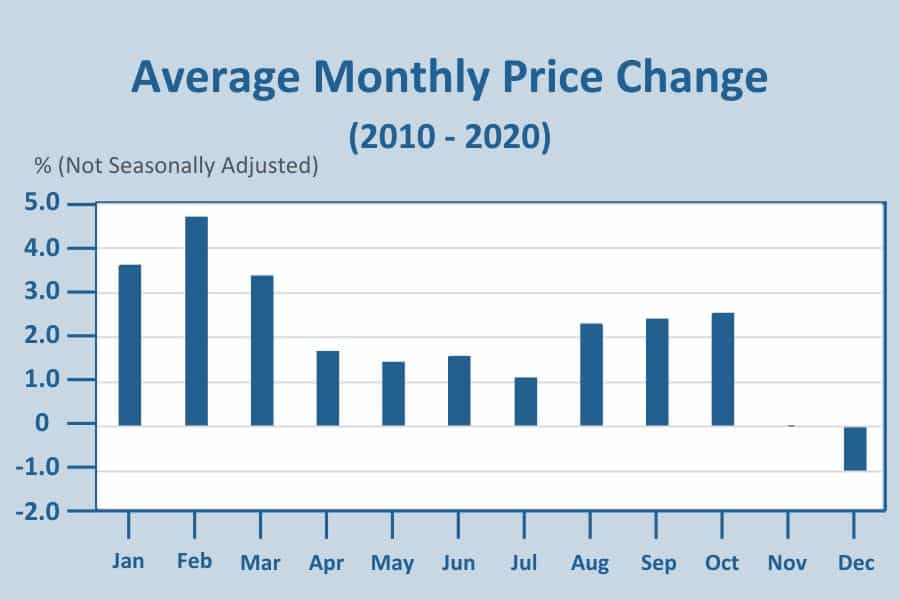

So why is the Fed downplaying the hotter inflation data over the past two months? Historically, the consumer price index in January and February increases faster than in any other month of the year. In the 10 years before the pandemic, the core consumer price index, which excludes volatile food and energy prices and is considered more representative of underlying inflation, increased by an average of 4.1% at an annual rate, much higher than every subsequent month and more than double the 1.5% average from March through December.

One reason is that businesses reset prices in January to cover wage and other cost increases incurred over the previous year. While this is a recurring phenomenon, statisticians usually do not entirely remove the early-year price bump through the seasonal adjustment process. This statistical quirk extends into February because the Labor Department collects data for certain items every other month, depending on the goods and services and their location. The reliability of the winter readings is further diluted by unpredictable weather conditions, which were particularly harsh this January and may have depressed the response rate in the survey, pushing some outsized price increases into February.

That said, the Federal Reserve’s board of directors was undoubtedly irked by the upside inflation surprise, supporting their decision to hold off on rate cuts. Some still believe holding rates “higher for longer,” which is now the Fed’s playbook, runs the risk of overstaying a restrictive policy, sending the economy into a recession. However, policymakers believe that the ongoing strength in the job market diminishes that risk, particularly since wages are rising at a solid clip, generating the purchasing power to support consumption. As long as consumers continue to spend – which drives about 70% of total economic activity – the downturn risk is slim.

Strong Hiring Will Not Derail Rate Cuts

That, of course, is where the rubber meets the road. Just as inflation and job growth became surprisingly hot, consumers turned more frugal than expected to start the year, as retail sales slumped in January and February. The early-year hiatus may be nothing more than consumers taking a breather following their shopping spree over the holidays in the final months of 2023. Moreover, although they are shunning goods sold at retailers, households still spend on services — traveling, attending concerts (hello Taylor Swift), sporting events, and generally partaking of experiences avoided during the pandemic.

From our lens, consumers are not about to zip up their wallets and purses as real incomes are growing at a decent pace, thanks to solid job growth, and households, in the aggregate, are in good financial shape. Nor does the strength in the job market cause much of a concern to policymakers, despite the potential wage-price spiral that an overly tight labor market threatens to bring about. As Fed Chair Powell noted at the latest post-meeting press conference, the steepest decline in inflation last year occurred alongside accelerated job growth. The economy’s strength last year was driven as much by expanded supply as demand. Goods became more available, immigration boosted the labor supply, and people returned to the labor force.

The Fed is counting on more supply-driven growth to continue easing wage and price pressures this year, paving the way for rate cuts. That’s why the upgraded forecast presented at the March 20 policy meeting included a higher growth outlook with only a modest uptick in inflation expectations. That said, the Fed is understandably coy about when it expects to start the easing process, setting the stage for months of speculation in the financial markets that could spur higher-than-average volatility.

We agree that the firm readings on prices early in the year overstates actual inflation, and the trend is likely heading lower. Besides the seasonal quirks mentioned earlier, there is a lot of disinflation in the pipeline, particularly for goods, and the elevated pace of housing costs – which had a significant influence on the January & February inflation data – does not capture the considerable slowing of market rents currently unfolding. They will, however, soon enter the official data and drag down the inflation rate later in the year. The widespread expectation is that the first rate cut will likely come in June or July, a timetable that seems appropriate. By then, the Fed will have three more reports on inflation and jobs, which should give a more accurate picture of where the economy stands — and what policy changes will be needed. The wintry mix of noisy data will soon give way to more clarity as normal weather and price-setting conditions return.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

The information contained herein is for informational purposes only and does not constitute a recommendation or advice. Any opinions are those of Legacy Private Trust Company only and represent our current analysis and judgment and are subject to change. Actual results, performance, or events may differ based on changing circumstances. No statements contained herein constitute any type of guarantee, nor are they a substitute for professional legal, tax, or other specialized advice.